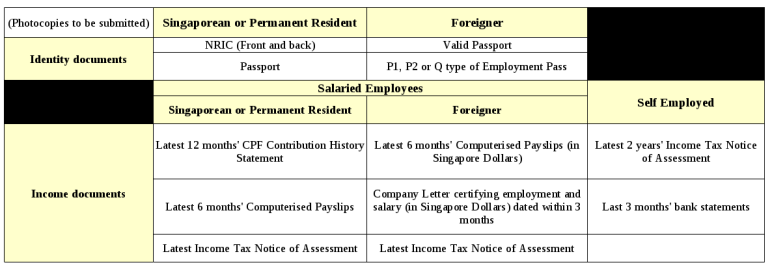

Here, we will take a look at some of the main types of loan products available in Singapore and a few important points that you should keep in mind while going in for these loans:

Personal Loans

These are multi-purpose, non-collateralize borrowings. They are usually high-interest loans, higher than home or car loans but not as high as credit card borrowings.

A personal loan, used well and repaid on time, can actually help you build credit. If you are finding it difficult to get a personal loan from a mainstream bank, you may approach a moneylender. If borrowing from a moneylender check the Ministry of Law’s Registry of Moneylenders to see if your moneylender is authorized and also the Ministry’s informative “Guide to borrowing from moneylenders”.

Car Loans

Buying a car in Singapore can be an expensive affair; next only to a home loan. Consider this: in addition to the Open Market Value (OMV) of the car, you will have to pay a tiered Additional Registration Fee that may go up to 180% of the OMV. Of course, there is the all-important Certificate of Entitlement (CoE). And, the Goods and Services Tax, Excise Duty, Road Tax and Parking Fees add the icing to the cake!

Remember, also that loans for vehicles with an OMV of up to S$20,000 will be limited to 60% while loans for vehicles with an OMV of more than S$20,000 will be capped at 50%.

Given all the above, a second-hand car may remain a good option for you. They are cheaper, have lesser waiting time, no CoE bidding and small transfer fees. PARF (Preferential Additional Registration Fee) second-hand cars that are eligible for both PARF and CoE rebates are preferable to CoE cars which are eligible only for the CoE rebate.

Of course, you must do the basic checks: test drives, getting a mechanic to go over the car and even getting the car over to a trusted third party workshop for inspection.

Home Loans

The questions uppermost on a would-be home loan borrower’s mind usually are:

How much can I afford? This will depend upon two variables:

The Total Debt Servicing Ratio (TDSR) – This is the ratio of your income and liabilities. The Monetary Authority of Singapore (MAS) has capped TDSR on property loans to 60% to encourage prudent borrowing.

Loan-to-Value (LTV) ratio – This is the ratio of the amount of loan taken against the value of the property expressed in percentage terms. Since the introduction of the TDSR framework for property loans by the MAS, which came into effect from the 29th of June 2013, the maximum Loan to Value (LTV) that can be borrowed is 90% depending upon the type of property.

Most banks have eligibility / repayment calculators on their websites. Use them to get an idea of how much you can afford and what your repayments will be like.

Check Your Home Loan Repayment Calculator in Citibank Singapore Website.

Do I go in for a new or an existing home?

This will depend upon the following points:

- Maximum tenor – The maximum tenor of home loans is restricted to: 30 years for HDB flats and ▪ 35 years for private properties

- Type of property / type of loan (if you are a first-time buyer with no outstanding home loan)

HDB Flat with a HDB loan – You can borrow up to 90% of the value of the home and use your CPF savings to pay off the 10% down payment provided the loan tenor is capped at 25 years.

HDB Flat with a bank loan – You can borrow up to 80% of the value of your home and use your CPF to pay 15% of the remaining and pay the other 5% in cash; loan tenors are longer at 30 years.

Furthermore, buyers of resale HDB flats have to fork out an additional COV (cash over value), which can amount to as much as $50,000, and has to be paid out to the seller in cash.

Private properties – Loans are available from banks; if the tenor does not exceed 30 years and the loan does not extend beyond 65 years, an LTV of up to 80% can be obtained; 5% of the remaining to be paid in cash and the remaining can be paid with CPF savings. If the loan tenor exceeds 30 years or if the loan extends beyond 65 years, only 60% LTV can be obtained.

What kind of a home loan should I take? There are two main types of home loans available:

Fixed Rate Home Loans – A fixed rate of interest is applied for the first few years (period may vary from bank to bank); thereafter the loan is converted to a floating rate. You may also be “locked” to the loan for the duration that it is fixed. Refinancing or making partial/full prepayments during the lock-in period could result in hefty penalties, of the total amount refinanced or prepaid.

A fixed rate will protect you from volatility but will also prevent you from taking advantage of rate drops.

Floating Rate Home Loans – These are usually tied to a reference interest rate (usually SIBOR or the Singapore Interbank Offered Rate, SOR or the Singapore Swap Offer Rate or the IBR or the Internal Board Rate which is fixed by your bank). Your monthly repayments may vary depending upon movements to the reference rate. There are floating rate products that come with / without lock-in periods.

Ideally you should choose between SIBOR-based and SOR-based loans, which are more transparent and not subject to the banks’ discretion.

Floating rate loans will always involve interest rate volatility. A way to mitigate this is to opt for a longer tenor SIBOR or SOR. For example, a 12-month SIBOR or SOR rates is revised every 12 months, so you get to enjoy fixed rate for a year!

We’ve already discussed briefly about overview of Home Loan.

Business Loans

There are various types of business loans available for you, if you have a business. These loans could help you to expand and improve, meet cash-flow requirements and purchase necessary equipment / supplies. These include Working Capital Loans, Factoring Loans, Short-term Loans, Overdraft and Hire Purchase Loans.

Other avenues for raising funds include Equity Financing and Collateralize Loans. If you have a start-up business, you may need to rely on your own personal credit sources. There are also a few micro finance options available in Singapore:

A collaboration between POSB Social Enterprise Hub Ltd (SE Hub Ltd, a social enterprise that seeks to invest in and incubate social enterprises) and the Singapore Totalisator Board (“Tote Board”), the MicroCredit Business Scheme (MCBS) is designed to provide those earning less than $30,000 a year the chance to take unsecured loans to start or expand their small businesses including food stalls, retail shops or hair salons. The loans can be from $3,000 to $50,000 with interest rates as low as 8 percent a year. MCBS officials will guide the loan applicants on business skills.

SPRING Singapore, an agency under the Ministry of Trade and Industry, offers a Micro Loan Programme of up to S$100,000 for daily operations or for automating and upgrading factory and equipment. These are available to companies registered and operating in Singapore with at least 30% local shareholding and with less than or equal to 10 employees or annual sales of less than or equal to S$1million. Interest rate is generally a minimum of 5.5% for loan tenors of 4 years and below.